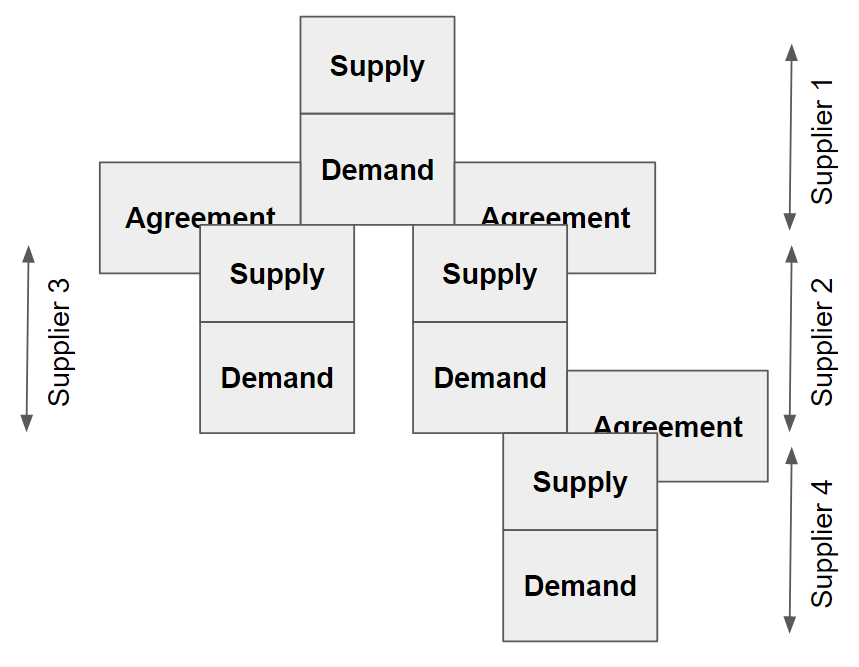

Supply and demand is the foundational theory of how prices and quantities are set in a market economy. It holds that the price of a good settles at the point where the amount that sellers are willing to supply equals the amount that buyers are willing to buy. Simple to state and remarkably powerful, it is the first thing taught in economics and the framework through which economists understand markets of every kind.

The theory rests on two opposing forces. Buyers tend to want more of a good when its price is lower and less when it is higher, which is the law of demand. Sellers tend to offer more when the price is higher and less when it is lower, the law of supply. These pull in opposite directions, and the market price gravitates toward the level where the two are in balance, coordinating the choices of countless buyers and sellers without any central direction.

At the equilibrium price, the quantity buyers wish to purchase exactly matches the quantity sellers wish to provide, and there is no pressure for the price to move. If the price is too high, unsold goods pile up and sellers cut prices; if too low, shortages appear and prices rise. This self-correcting tendency, represented in the famous crossing of the supply and demand curves, was given its now-standard graphical form by the economist Alfred Marshall.

The theory also predicts how markets respond to change. A new technology that makes a good cheaper to produce increases supply and tends to lower its price; a surge in popularity increases demand and tends to raise it. These predictions are borne out constantly in real markets, from the price of crops after a good harvest to the cost of goods in short supply, which is much of why the theory is so trusted.

The basic model assumes many buyers and sellers, good information, and competition, and economists actively debate how well it describes the messier real world. Monopolies, advertising, costs imposed on third parties such as pollution, and the quirks of actual human behaviour can all pull markets away from the simple prediction. These complications refine rather than overturn the theory, which remains the indispensable starting point for understanding prices.

For all the debate about its limits, supply and demand is the bedrock on which economics is built, a lens applied to everything from labour and housing to interest rates and global trade. Few ideas in the social sciences are at once so simple, so widely used, and so consistently illuminating.